Chart 1: Current Global Energy Mix Global primary energy consumption by source

Primary energy is calculated based on the 'substitution method' which takes account of the inefficiencies in fossil fuel production by converting non-fossil energy into the energy inputs required if they had the same conversion losses as fossil fuels.

Source: Our World in Data.org, BP Statistical Review of World Energy

The chart above shows how our current energy load is provided for. Hydrocarbons account for nearly 65% of our daily energy consumption. Pre-pandemic oil demand was growing at approximately 1m-1.5mn barrels per day. Simultaneously, global oil reserves deplete at approximately 8% per annum – meaning we have to find approximately 8mn barrels per day per year to maintain current reserves. The Shale Oil revolution began in earnest in 2011, which initially contributed to a significant global weakness in crude prices, averaging 40 -60USD per barrel between 2014 and 2021. In fact, few realise that now the US is the biggest producer in the world – at nearly 10mn barrels per day, dwarfing Russian and Saudi daily output. However, that was before the ESG movement catalysed a massive curtailment in financial capital available to US shale oil projects, for which we are now beginning to feel the effects. As new supply projects have been shelved, due to little appetite on behalf of banks or investors, demand continues its inexorable push higher, and the markets have tightened.

If we were to simply stop drilling now, effectively go cold turkey, then within two decades we would need to find another 7 Shale Oil discoveries, or perhaps even more starkly, another 7 Saudi Arabia’s to fill the supply void. J. P. Morgan has just released a doomsday report pricing oil at 380 USD should Russian oil be sanctioned, which entails removing entirely 4.5mn or say barrels of crude per day from the market. Anybody with an electricity bill would shudder (or more likely shiver), if faced with energy prices resulting from an effective prohibition on all hydrocarbon based fuels.

Over the next decade the world is due to add 1.1bn people according to the United Nations, all of which will require more energy, rather than less. Electrifying the world – transitioning from molecules to power, will also bring significant transmission challenges. The capacity required will mean ultra efficient energy grids – whereas in the West, our current infrastructure would be charitably described as antiquated.

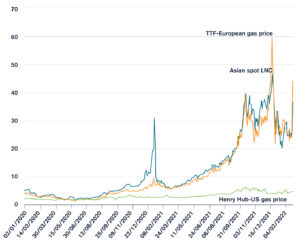

European Dependency Chart 2: Europe currently facing gas prices equivalent to 600 USD oil

Source: IEA.org, ARIA

Source: IEA.org, ARIA

Russia’s invasion of Ukraine puts Europe under acute pressure. As of June 2022, Europe currently digests a gas price that is 6-8 times that which the US pays. That in and of itself puts any energy intensive industry at a significant cost disadvantage to its global peers – Germany is a manufacturing powerhouse and we would expect it already to be in recession with such high input costs. Not to mention the profound impact that those prices have on the European consumer. It’s not surprise that Spain has announced 6bn EUR support plan in direct aid, tax breaks and fuel subsidies to cushion the blow, Italy 3bn EUR and Germany is having to nationalise Uniper one of its biggest gas uitility companies on account of the losses sustained by rising gas prices.

Oil is more fungible than gas as a commodity. Germany only imports 20% of its oil from Russia, and so it is easier to consider oil sanctions. However, Putin’s pipelines are responsible for 40% of Germany’s gas. Replacing Russian natural gas supplies is more problematic that crude. To transport gas means liquified natural gas, or LNG, which requires liquification, then freezing to minus 160 degrees centrigrade, before loading specially designed vessels before re-liquifying again at the destination port. LNG port infrastructure requires investments of between 15 to 50 billion USD and typically 4 years to complete – assuming permissioning can be achieved within 12 months.

The Rise of the Chinese Dragon

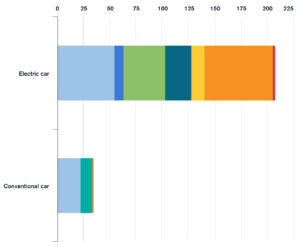

Measuring the carbon and financial cost of renewables perhaps is to tell some of the story – it doesn’t necessary account for the full lifecycle of the technologies. In some respects, it is the ‘inconvenient truth’ of green technologies – namely that their construction is highly reliant on minerals and metals – which means energy intensive mining and extractive resources once more. The new sustainable world is largely dependent on metals found in minute quantities, bursting with remarkable properties, which are referred to as ‘rare earth’ metals. Wind turbines, solar panels and electric cars and their decarbonised energy, require significant quantities of metals, which form a family of seventeen elements, all with exotic names such as antimony, germanium, indium, tungsten and gallium. These rare earths all possess supreme electromagnetic, catalytic and chemical properties. Transitioning our energy model will mean doubling rare metal production every fifteen years. In fact, it is anticipated over the next thirty years we will need to mine more mineral ores than humans have extracted over the last 70,000 years. As with any mining activity, the process of extraction requires staggering quantities of water, which then are often polluted by heavy metal concentrates and chemicals in the leaching process, moreover, often then entering the water table feeding local communities. China is the major producer for nearly 28 rare earths that have been deemed fundamental to our digital and sustainable futures – often accounting for more than 50% of exported volumes. Rare earths are concentrates, and very resource intensive – it takes 8.5 tonnes of rock to be purified to produce a kilogram of vanadium; sixteen tonnes for a kilo of cerium, fifteen tonnes for the equivalent in gallium. Great Britain’s dominance in the nineteenth century is often attributed to its pre-eminence in coal production, the more recent hegemony of the United States could be viewed through its relationship with Saudi to safeguard oil supplies before achieving energy independence in its own right. Controlling the means of energy production, access to and its cost goes a long way to economic sovereignty. As we stand there is one state better positioned than any to do so in rare earths: the Middle Kingdom. That’s not to understate the importance of perhaps Rwanda to tantalum, and the Democratic Republic of Congo to cobalt, but again, typically they are produced from Chinese mines. We expect that in the years to come, particularly if the current geopolitical tensions continue to redraw the map of ‘friends and foes’, that there will be ever greater scrutiny of supply chains and their provenance. Moreover, to date the success of recycling rare earth metals has been very underwhelming. Therefore, when the reliance on oil changes to an addiction to rare earth metals, and the potential for national security issues to result, we feel that there will be pause for thought along the way.Chart 3: Minerals used in electric cars compared to conventional combustion engine

Source: ARIA, IEA.org

Source: ARIA, IEA.org

At ARIA Commodities, we believe we have strong ‘environmental credentials’. From our carbon neutral fuels trading, or financing of certified avocado production, with zero fertiliser production and farmer education programs, through to our recycled lead battery interests in East Africa, our renewable investing platform and our corporate program of natural carbon offsets, we have mapped a number of ways to reduce our carbon footprint to zero in the coming years. A true net zero where possible. Moreover, we believe we can positively steer capital towards ensuring the energy transition to a greener future. We’re pragmatic about what that energy mix looks like, but also fervent believers in newer or proven technologies which will make a significant contribution to achieving these noble goals.

ARIA Commodities