December 2023

Global coal production: supply outlook in energy transition?

Perhaps surprising to many, global coal production likely saw a new all-time peak of 8.7GTpa in 2023, of which 7.5GTpa is thermal coal and 1.2GTpa is metallurgical. The largest producers details China at approximately (4.4GTpa), India (1GTpa), before other Asian producers turn out (0.7GTpa, finally European and US mines supplying approximately 0.5Gt each.

Coal in most circumstances can be the cheapest thermal energy source on the planet. Formed by thousands of years of geological transformation of organic materials, in normal times, it can cost $60/ton and contains 6,250 kWh/ton of thermal energy, implying a cost of 1c/kWh-th. That is significantly below most sources of power, although of course it is not a çarbon adjusted metric in any way.

By extension, coal-fired power can thus cost 2-4c/kWh and an existing coal plant is cheaper than other levelised costs of power. Coal is clearly the highest-carbon fossil fuel, with an average CO2 intensity of 0.37 kg/kWh-th, which is 2x more than gas.

The additional CO2 burden is exacerbated when considering coal’s Scope 1+2 emissions, as often coal mining leaks more methane than gas itself. Moreover, in power installations that use Rankine steam cycles fuelled by coal have efficiency drawbacks, not to mention relatively low flexibility.

Various commentators in their roadmaps to net zero would need to see coal consumption flat-lining from 2022, then declining at 8% pa in the 2030s and 17% pa in the 2040s, to well below 500MTpa. However, we find that difficult to hold, unless the ramp up in renewables, wind and solar, and ‘stepping stone energy sources, natural gas, are ramped up enormously.

It’s true to see how certain geographies are pointing to flatlining production, namely the US, where coal production peaked at 1GTpa in the 2010s, before shale gas ramped to 80bcfd. Thus US coal declined to 500MTpa in 2021. Although questions about the continued phase-back of US coal are now being raised, due to pipeline bottlenecks from the Marcellus, and the European energy crisis, requiring a substitution of Russian energy supplies (oil, coal and gas).

When energy markets are not in balance, precipitated by events such as the Ukrainian invasion in 2022, international coal prices, along with the entire energy spectrum, will spike – in coal’s case to over $340/ton. Remarkably, this took thermal coal prices above metallurgical coal, and even above oil on a per-btu basis.

Metallurgical coal may be particularly challenging to substitute. For example, green steel economics, (whilst many technologies are still early stage), are challenging although bio-coke provides for some interesting opportunities. The gasification of coal into hydrogen at economic cost also raises questions, although Chemical Looping Combustion, offers significant opportunities to derive high value fuels.

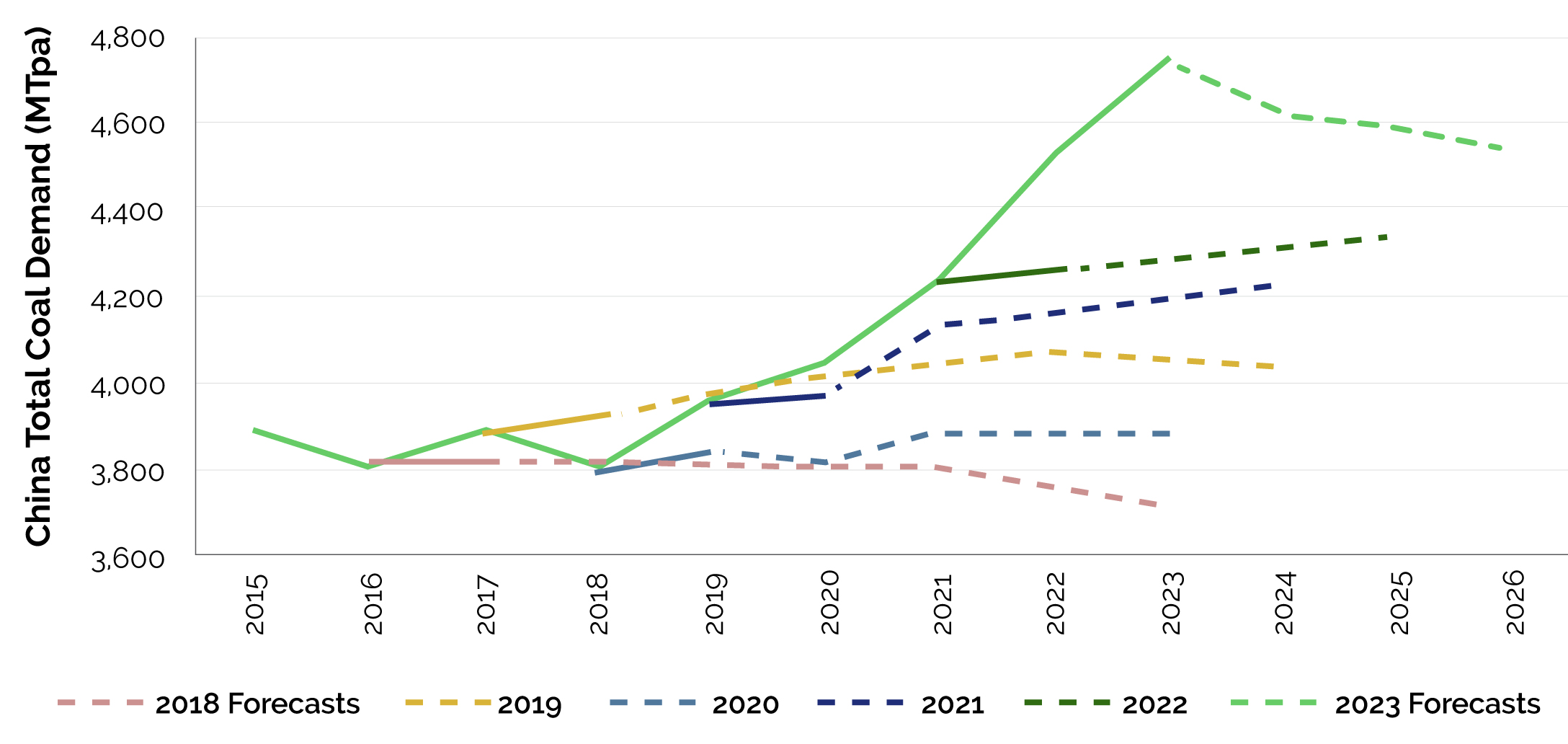

Around 1GTpa of new coal projects are in planning or under construction, of which half are in China. Chinese coal production is something of a ‘wildcard’, and along with India, have made no secret of their plans to continue to keep the lights on using thermal coal power plants. The Japanese alone, whilst developing plans to co-fire their coal power plants with Ammonia, and having pledged to achieve net zero ambitions by 2050, still will import over 100mn tonnes in 2024. Despite rising renewables, coal demand continues to defy expectations:

Source: ARIA, ThunderSaid Energy, Technical Papers

China imports every third tonne of coal sold globally, yet India’s coal use has also doubled since 2007, rising at 6% pa. It remains “the engine of global coal demand”, according to the IEA, rising +70MTpa, to 1.1GTpa in 2022, 1.3GTpa in 2023 and 1.4GTpa in 2026.

Countries who are still developing cannot afford elevated energy prices – their economic growth depends on it. The ultimate transition for coal may not be its supply, but rather how it is produced and used – çlean coal technologies would thread the needle; not deprive emerging markets of cheap energy, whilst fundamentally resolving the carbon cost of thermal coal.