The Fourth Dimension:

Leveraging Scope 4 for surgical investments.

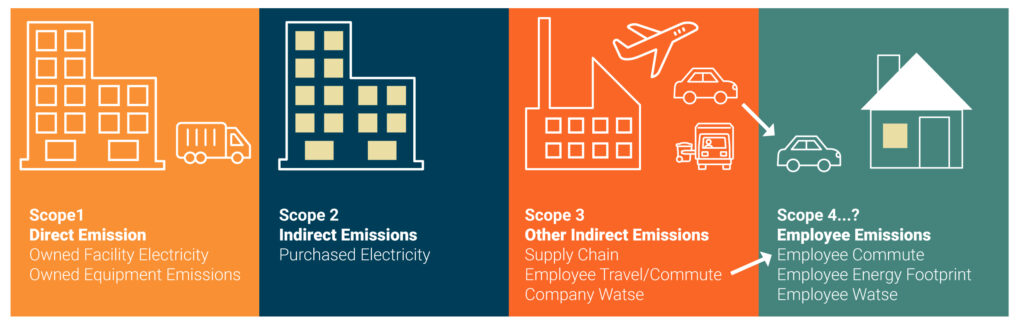

In the realm of greenhouse gas (GHG) emissions, companies traditionally categorize their environmental impact into three distinct scopes. Scope 1 encompasses direct emissions from a company's own operations, while Scope 2 includes indirect emissions from the energy it purchases. Scope 3, the most intricate, covers all other indirect emissions within a company's value chain, often constituting a significant portion of total emissions.

While measuring and reporting on Scope 1 and 2 emissions are relatively straightforward, Scope 3 presents a complex challenge due to potential double counting and the vast size and intricacy of the value chain. Scope 3, accounting for approximately three-quarters of a company's emissions, demands a comprehensive assessment up and down the supply chain, involving numerous suppliers and products.

Adding to this complexity, Scope 4 emissions introduce a new layer of intricacy. Scope 4 represents "avoided emissions" resulting from the production and use of more carbon-efficient products or services that sidestep carbon emissions. Proposed by the World Resources Institute (WRI) in 2013, Scope 4 encourages businesses to look beyond their immediate operations and consider the broader carbon benefits they may contribute to the global economy.

Incentives, whether monetary or reputational, predominantly focus on reducing Scope 1, 2, and 3 emissions. However, this singular focus may overlook innovations with substantial net emissions benefits for the global economy. For instance, while manufacturing electric batteries or wind turbines may have high energy and carbon intensity, their Scope 4 emissions could outweigh the emissions produced during their production.

For example, Vestas, a wind turbine manufacturer, estimates that its turbines, produced in 2021, will avoid 532 million tonnes of emissions over their operational lifetime. This far surpasses its annual Scope 1, 2, and 3 emissions of 100,000 tonnes, 3,000 tonnes, and 10.5 million tonnes, respectively.

Estimating Scope 4 emissions proves challenging, akin to the complexities faced by the carbon credit market. Over-crediting, or issuing more credits than actual emissions avoided, poses a significant risk. Questions around baseline emissions, comparison criteria, and the carbon intensity of energy sources need consistent answers for meaningful assessments.

Some companies may be tempted to leverage Scope 4 emissions to offset obligations related to Scope 1, 2, and 3 emissions. However, this approach is a non-starter, as Scope 4 emissions should ideally be accounted for within the existing scopes, by other entities in the economy.

Nevertheless, recognizing and rewarding innovation with broad-based net-zero benefits has sparked interest among companies. Those with carbon-intensive operations may find appeal in showcasing the broader carbon benefits their products enable, attracting sustainability-oriented investors.

Traditional sustainable investment strategies often involve divesting from high-emission companies and redirecting capital towards low-emission counterparts. This strategy, while reducing the cost of capital for high-emission firms, may inadvertently impede their ability to decarbonize. Recognizing the importance of Scope 4 emissions introduces a paradigm shift, emphasizing not just what a company emits but also what it enables others to avoid.

In essence, Scope 4 emissions add value by acknowledging the contribution made in avoiding emissions, aligning with the efficiency principle in carbon abatement. It reframes the narrative from a universal burden on each entity to a strategic allocation of efforts where high-cost emitters support those with greater potential for emission reduction. Acknowledging the value of avoided emissions may redefine the landscape of emission accounting and incentivize a more nuanced and effective approach to achieving net-zero goals.